Illustration by NanoBanana

Illustration by NanoBanana

A vacant one-bedroom on March 1st and an idle H100 at 2 AM share the same brutal economic truth: the revenue from that moment is gone forever. The rent you didn’t collect last month and the compute you didn’t sell last hour are both inventory that perished on the shelf. Fixed costs — the mortgage payment, the power bill for the cooling system — don’t care whether anyone showed up.

This isn’t a cute analogy. It’s the same problem, and increasingly, both industries are arriving at the same solutions.

Two Markets, One Structure

The parallels between GPU cloud compute and multifamily housing run deeper than you might expect.

Both sell time-bound capacity. An apartment is really a bundle of unit-months. A cloud GPU is a bundle of GPU-hours. Neither can be warehoused. If a 300-unit property runs at 93% occupancy, those 21 vacant unit-months each month are revenue that will never come back. If a rack of NVIDIA B200s — representing millions of dollars in upfront hardware cost — sits at 40% utilization, the idle hours are burning cash at a staggering rate.

Both face agonizing supply lags. New apartment construction takes 18 to 24 months from groundbreaking to first lease-up. New GPU fabrication capacity takes two to three years to come online. The result in both cases is boom-and-bust cycles where supply overshoots or undershoots demand by the time it arrives.

Both experience demand volatility. Multifamily leasing follows seasonal patterns — summer peaks, winter troughs — overlaid with macro cycles of job growth and migration. GPU demand spikes around major model training runs, new chip launches, and shifts between training and inference workloads. The amplitude is different (GPU demand can move 10x overnight when a new foundation model drops), but the shape is the same.

Both use price as the primary balancing mechanism. And this is where the convergence gets interesting.

The Data Tells the Same Story

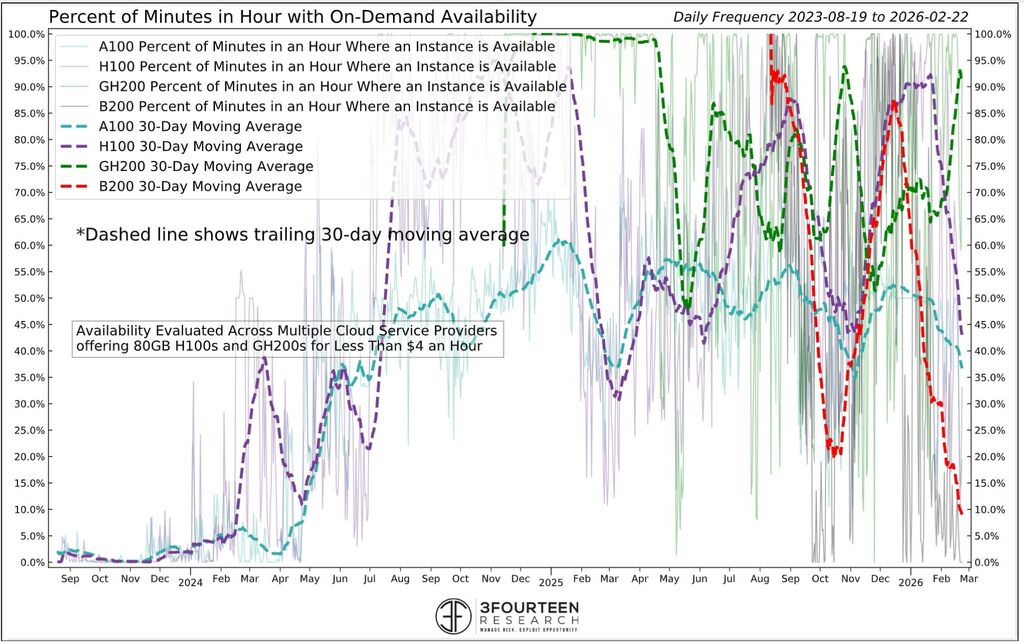

On the GPU side, the pattern is vivid. 3Fourteen Research tracks real-time on-demand GPU availability across cloud providers, and their data shows wild cyclicality. Through late 2023 and early 2024, on-demand availability for H100s was near zero — you simply couldn’t get one. By mid-2025, supply caught up: H100 and GH200 availability surged to 80–90% as new capacity came online. Then Blackwell arrived, demand exploded again, and by early 2026, availability for the newest GPUs collapsed back toward zero. The chart looks less like a steady-state market and more like a seismograph.

GPU on-demand availability across cloud providers, Aug 2023 – Feb 2026. Note the wild swings from near-zero to 90%+ and back. Source: 3Fourteen Research

GPU on-demand availability across cloud providers, Aug 2023 – Feb 2026. Note the wild swings from near-zero to 90%+ and back. Source: 3Fourteen Research

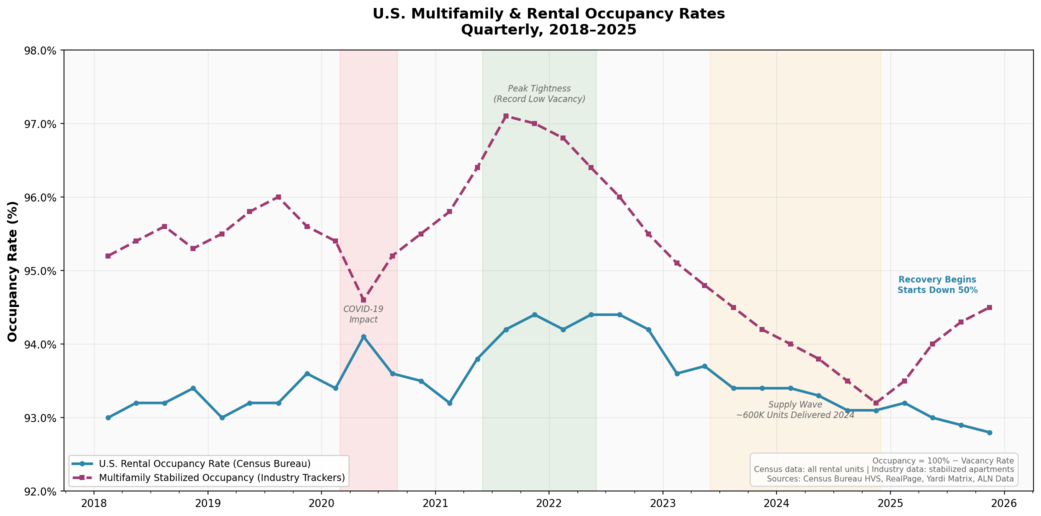

The multifamily market tells a remarkably similar story, just on a slower timescale. Developers delivered nearly 600,000 new apartment units in 2024 — the most since 1974 — with the Sun Belt absorbing a disproportionate share. Charlotte grew its apartment stock by nearly 8% in a single year; Austin exceeded 10%. The predictable result: occupancy softened, and advertised rents in Sun Belt markets turned negative — Austin down over 3%, Phoenix down over 4%, Denver nearly 2%. It was the apartment equivalent of the mid-2025 GPU glut — supply finally arriving just as the market had already repriced expectations.

U.S. rental and multifamily stabilized occupancy rates, 2018–2025. The same boom-bust cycle plays out — just measured in quarters instead of minutes. Sources: Census Bureau HVS, RealPage, Yardi Matrix, ALN Data

U.S. rental and multifamily stabilized occupancy rates, 2018–2025. The same boom-bust cycle plays out — just measured in quarters instead of minutes. Sources: Census Bureau HVS, RealPage, Yardi Matrix, ALN Data

But here’s the parallel that matters most: both markets are now past peak supply. Multifamily construction starts have fallen nearly 50% from their cycle high, and occupancy is recovering. GPU availability for the latest Blackwell chips is back to near-zero as demand from hyperscalers, enterprises, and AI startups overwhelms everything NVIDIA and its partners can ship. In both cases, the clock resets and the scarcity cycle begins again.

The Revenue Management Convergence

Faced with the same core problem — perishable inventory with volatile demand — both industries have converged on the same solution: algorithmic revenue management.

Multifamily operators now use platforms like Yardi Revenue IQ, RealPage, and newer entrants to dynamically price every unit based on real-time occupancy, seasonal patterns, local comps, and lease expiration curves. The goal isn’t to maximize the rent on any single unit; it’s to optimize total revenue across the entire portfolio, balancing occupancy against rate. A property might accept a lower rent to avoid a vacancy that would cost more in lost revenue than the discount.

GPU cloud providers have arrived at the same logic through a different door. Reserved instances function like long-term leases — a commitment discount in exchange for guaranteed occupancy. Spot pricing is the equivalent of last-minute apartment deals: deeply discounted, but you might get evicted (preempted) if someone pays full price. On-demand pricing is the walk-in rate, the month-to-month lease — maximum flexibility, maximum cost. The pricing tiers map almost perfectly.

Both are playing the same game: control demand through price inflection to maximize yield on a finite, time-sensitive asset.

Where the Analogy Breaks

The comparison isn’t perfect. GPU workloads can materialize and vanish in seconds; tenants sign 12-month leases that provide a revenue floor multifamily operators can plan around. A single customer announcement — say, a hyperscaler deciding to pre-train a new frontier model — can absorb thousands of GPUs overnight in a way that has no apartment-market equivalent.

And GPU supply has a flexibility lever that apartments lack: software. Multi-tenancy, fractional GPUs, and workload scheduling can effectively expand capacity without building anything new. You can’t split a one-bedroom into two half-bedrooms (legally, at least).

The Lesson

But these differences are matters of degree, not kind. Both industries are learning the same fundamental lesson: when your inventory perishes every hour — or every month — the management of utilization is the business. The building is not the product. The GPU is not the product. The occupied hour is the product.

Whether you’re running a 300-unit apartment complex or a 10,000-GPU cluster, the playbook is converging: forecast demand, price dynamically, minimize vacancy, and accept that the real enemy is always the clock.

Sources: 3Fourteen Research GPU availability tracker · 24/7 Wall St. on near-zero GPU availability · CIO Dive on data center capex · CBRE U.S. Multifamily Outlook · Cushman & Wakefield U.S. Multifamily MarketBeat · Census Bureau Housing Vacancies & Homeownership via FRED